Types, Interest Rates & How to Choose the Best One in 2026

Managing your finances effectively begins with selecting the appropriate bank accounts in India. With numerous banking options available across the country, understanding the various types of bank accounts in India becomes crucial for making informed financial decisions that align with your specific needs and goals.

This comprehensive guide explores everything you need to know about bank accounts in India, covering savings accounts, fixed deposits, current accounts, minimum balance requirements, interest rates, and digital banking services. Whether you’re new to banking or seeking to optimize your financial management strategy, this guide provides valuable insights into India’s banking landscape.

Understanding Bank Accounts in India: The Foundation of Financial Management

Bank accounts in India serve as the cornerstone of personal finance management, offering secure platforms for storing money, earning interest, and conducting daily transactions. The banking sector in India has evolved significantly, incorporating advanced digital technologies while maintaining traditional banking strengths.

Modern banking institutions provide diverse account options designed to meet varying financial requirements, from basic savings needs to complex business transactions. Understanding these options helps individuals and businesses choose accounts that maximize benefits while minimizing costs.

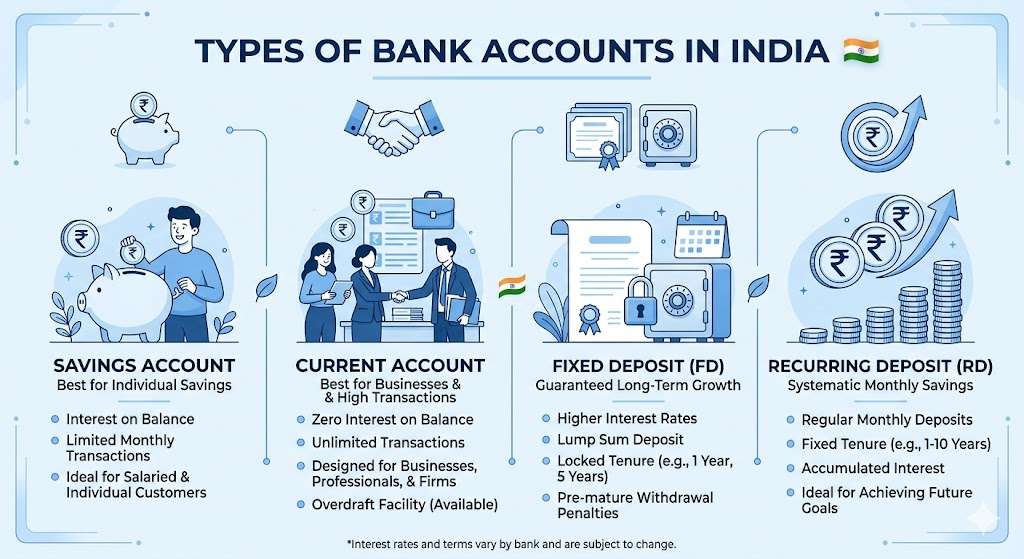

Types of Bank Accounts in India: A Detailed Overview

The Indian banking system offers several distinct types of bank accounts in India, each designed to serve specific financial purposes and customer segments.

1. Savings Accounts: The Most Popular Choice

Savings accounts represent the most widely used bank accounts in India, serving millions of customers across urban and rural areas. These accounts provide a perfect balance between accessibility and interest earnings.

Key Features of Savings Accounts:

- Secure money storage with guaranteed protection

- Regular interest payments on deposited amounts

- Convenient access through ATMs, online banking, and mobile apps

- Debit card facilities for cashless transactions

- Mobile banking and UPI payment integration

- Overdraft facilities in premium accounts

If you are looking for credit-based banking options, you can also explore our detailed guide: What is Credit Card? Complete 2026 Guide to Meaning, Types and Benefits

Read More: 7 Hidden Benefits of Axis Myzone Rupay Credit Card in 2026

Interest Rates for Savings Accounts:

Current savings account interest rates in India typically range between 2.5% to 7% annually, depending on the bank type and account variant. Small finance banks often provide higher interest rates compared to traditional commercial banks.

Top Banks Offering Competitive Savings Rates:

- State Bank of India (SBI)

- HDFC Bank

- ICICI Bank

- AU Small Finance Bank

- Ujjivan Small Finance Bank

- Kotak Mahindra Bank

For example, check our detailed guide on Small Finance Bank Savings Account Interest Rate 2026 to understand which banks offer the highest returns.

Some banks also offer better returns through fixed deposits. Check our guide on Updated SBI FD And Savings Ac Rates 2026

2. Current Accounts: Designed for Business Operations

Current accounts cater primarily to businesses, professionals, and individuals requiring frequent transactions. These accounts offer unlimited transaction facilities but typically don’t provide interest on deposits.

Features of Current Accounts:

- Unlimited deposit and withdrawal transactions

- Higher cash handling limits

- Overdraft facilities for business needs

- Checkbook facilities

- Business banking services

- Trade finance support

3. Fixed Deposit Accounts: Guaranteed Returns

Fixed Deposit (FD) accounts offer guaranteed returns for predetermined periods, making them popular investment choices among conservative investors.

Benefits of Fixed Deposits:

- Higher interest rates than savings accounts (typically 6% – 8%)

- Guaranteed returns with bank backing

- Flexible tenure options from 7 days to 10 years

- Loan against deposit facilities

- Tax-saving FD options under Section 80C

- Auto-renewal features

4. Recurring Deposit Accounts: Systematic Savings

Recurring deposits encourage disciplined saving through regular monthly contributions, offering attractive interest rates for systematic investors.

Key Features:

- Monthly deposit commitments

- Fixed tenure periods

- Interest rates similar to fixed deposits

- Penalty for missed deposits

- Automatic debit facilities

5. Salary Accounts: Employee-Focused Banking

Salary accounts serve employees receiving monthly salaries, often providing enhanced benefits and zero-balance facilities.

Special Benefits:

- Zero minimum balance requirements

- Higher transaction limits

- Personal loan pre-approvals

- Credit card offers

- Insurance benefits

Related Financial Guides You Should Read

If you want to make smarter financial decisions in 2026, these detailed guides will help you understand banking, credit cards, and investments better:

👉 Best FD Interest Rates in India 2026: Which Bank Gives Highest Returns?

👉 SBI Credit Card Minimum Due: Hidden Charges, Interest & Smart Payment Tips

👉 Credit Card Full Payment vs Minimum Due

These resources will help you choose the right bank account, avoid common financial mistakes, and plan your money wisely.

Minimum Balance Requirements in Bank Accounts India

Most bank accounts in India require customers to maintain minimum balance thresholds. Failure to maintain these balances results in penalty charges that vary across banks and account types.

Typical Minimum Balance Requirements:

| Bank Name | Urban Branches | Semi-Urban | Rural |

|---|---|---|---|

| SBI | ₹3,000 | ₹2,000 | ₹1,000 |

| HDFC Bank | ₹10,000 | ₹5,000 | ₹2,500 |

| ICICI Bank | ₹10,000 | ₹5,000 | ₹2,500 |

| PNB | ₹2,000 | ₹1,000 | ₹500 |

To understand the latest rules, read our detailed guide on SBI Savings Account Minimum Balance Essentials.

The minimum balance requirement may vary depending on the bank and account type. You can also check the official banking regulations on the Reserve Bank of India website.

Zero Balance Account Options:

Several banks offer zero-balance accounts under government schemes like Pradhan Mantri Jan Dhan Yojana, making banking accessible to economically weaker sections.

Fixed Deposits (FD) in India

A Fixed Deposit (FD) is a popular investment option offered by banks where money is deposited for a fixed period to earn higher interest.

Key Benefits

Higher interest rates than savings accounts

Guaranteed returns

Flexible tenure from 7 days to 10 years

Safe investment backed by banks

Typical FD interest rates:

Fixed deposits are one of the safest investment options offered by banks. They provide guaranteed returns and usually offer higher interest rates than savings accounts.

You can check the latest rates in our guide on SBI Fixed Deposit Interest Rate 2026.

Fixed deposits are one of the most popular investment options linked with bank accounts in India.

To compare current bank offers, read our latest post on best FD interest rates in India 2026.

Small Finance Banks: Higher Interest Rate Opportunities

Small finance banks have revolutionized bank accounts in India by offering competitive interest rates to attract customers from traditional banks.

Leading Small Finance Banks:

- AU Small Finance Bank: Up to 7% savings interest

- Ujjivan Small Finance Bank: Competitive rates with digital focus

- Jana Small Finance Bank: Rural and semi-urban specialization

- Equitas Small Finance Bank: Technology-driven services

- Suryoday Small Finance Bank: Customer-centric approach

These institutions often provide interest rates 1-2% higher than traditional banks while maintaining similar security standards.

Digital Banking Revolution in India

Modern bank accounts in India integrate advanced digital technologies, transforming how customers manage finances and conduct transactions.

Key Digital Banking Features:

UPI (Unified Payments Interface):

- Instant money transfers

- Bill payment facilities

- Merchant transactions

- QR code payments

Mobile Banking Applications:

- Account balance inquiries

- Fund transfers

- Fixed deposit bookings

- Loan applications

- Investment services

Internet Banking Services:

- Comprehensive account management

- Tax payment facilities

- Investment portfolio tracking

- Insurance premium payments

Digital Wallet Integration:

- Cashless transaction capabilities

- Reward point accumulations

- Multi-bank account linking

Digital banking has made it easier for people to manage their finances through mobile apps, UPI payments, and online banking services. To improve financial planning, you can also read our guide:

Personal Finance for Beginners: A Simple 2026 Guide to Managing Money.

How to Choose the Right Bank Accounts in India

Selecting appropriate bank accounts in India requires careful consideration of multiple factors that align with your financial objectives and lifestyle requirements.

1. Interest Rate Comparison

Higher savings interest rates significantly impact long-term wealth accumulation. Compare rates across different bank categories, including commercial banks, private banks, and small finance banks.

2. Minimum Balance Assessment

Choose accounts with minimum balance requirements that match your financial capacity. Consider penalty charges for non-maintenance before making decisions.

3. Digital Banking Capabilities

Modern banking demands robust digital infrastructure. Evaluate mobile apps, internet banking platforms, and UPI integration quality.

4. Customer Service Quality

Reliable customer support becomes crucial during banking issues. Research customer service ratings and response times.

5. Branch and ATM Network

Consider geographical coverage, especially if you frequently travel or live in multiple cities.

6. Additional Benefits

Evaluate insurance coverage, loan pre-approvals, credit card offers, and investment services provided by banks.

Benefits of Maintaining Multiple Bank Accounts

Strategic management of multiple bank accounts in India offers several advantages for comprehensive financial planning.

Advantages Include:

- Risk Diversification: Spreading funds across multiple banks reduces concentration risk

- Better Interest Optimization: Utilizing different banks for various purposes maximizes returns

- Enhanced Liquidity Management: Separate accounts for different financial goals

- Improved Emergency Planning: Multiple access points during bank-specific issues

- Specialized Banking Services: Different banks excel in different service areas

If you also need financial support, check our Complete Personal Loan Guide in India: Interest Rates, Eligibility & Tips (2026)

Smart Tips for Managing Bank Accounts in India

Effective management of bank accounts in India requires strategic approaches that maximize benefits while minimizing costs and risks.

Essential Management Strategies:

1. Maintain Required Minimum Balances

Consistently monitor account balances to avoid penalty charges that erode savings over time.

2. Leverage Digital Banking Securely

Use strong passwords, enable two-factor authentication, and regularly update banking apps for enhanced security.

3. Monitor Interest Rate Changes

Stay informed about interest rate fluctuations and consider switching accounts when better opportunities arise.

4. Optimize Transaction Patterns

Plan transactions to minimize charges while maximizing convenience and efficiency.

5. Regular Account Reviews

Conduct quarterly reviews of account performance, charges, and benefits to ensure optimal utilization.

Managing multiple bank accounts becomes easier when you use proper budgeting and planning tools. You can explore some useful financial planning tools in India to organize your savings and investments.

Advanced Financial Planning Integration:

Link bank accounts in India with systematic investment plans, insurance policies, and tax-saving instruments for comprehensive wealth management.

Latest Trends in Indian Banking Sector

The types of bank accounts in India continue evolving with technological advancements and changing customer expectations.

Emerging Trends Include:

Artificial Intelligence Integration:

- Personalized banking recommendations

- Fraud detection systems

- Automated customer service

Blockchain Technology:

- Enhanced security protocols

- Faster international transfers

- Smart contract implementations

Open Banking Systems:

- Third-party service integration

- Improved financial product comparison

- Enhanced customer control

Sustainable Banking:

- Green banking initiatives

- Carbon footprint tracking

- Sustainable investment options

Tax Implications of Bank Accounts in India

Understanding tax obligations associated with bank accounts in India ensures compliance while optimizing tax efficiency.

Key Tax Considerations:

Interest Income Taxation:

- Savings account interest up to ₹10,000 exempt under Section 80TTA

- Senior citizens get ₹50,000 exemption under Section 80TTB

- Fixed deposit interest fully taxable

TDS on Bank Deposits:

- 10% TDS on interest exceeding ₹40,000 annually

- Higher rates for non-PAN holders

- Form 15G/15H for lower income individuals

Future of Bank Accounts in India

The landscape of bank accounts in India continues transforming with technological innovations, regulatory changes, and evolving customer preferences.

Expected Developments:

Enhanced Digital Integration:

Banks will further integrate artificial intelligence, machine learning, and blockchain technologies to provide personalized, secure, and efficient banking experiences.

Increased Financial Inclusion:

Government initiatives and technological advancement will expand banking access to underserved populations across rural and urban areas.

Sustainable Banking Growth:

Environmental consciousness will drive banks toward sustainable practices and green banking solutions.

Conclusion: Maximizing Your Banking Experience in India

Choosing the right bank accounts in India forms the foundation of successful financial management. Understanding the various types of bank accounts in India empowers individuals to make informed decisions that align with their financial goals, risk tolerance, and lifestyle requirements.

Whether you prioritize higher interest rates from small finance banks, comprehensive services from large commercial banks, or specialized features from digital banks, the key lies in matching account characteristics with your specific needs.

The Indian banking sector offers unprecedented opportunities for wealth creation, financial security, and convenient money management. By leveraging digital technologies, understanding minimum balance requirements, comparing interest rates, and maintaining strategic account portfolios, individuals can optimize their banking relationships for long-term financial success.

Regular review and optimization of your bank accounts in India ensure you continue benefiting from the best available options as the banking landscape evolves. Stay informed about new products, changing regulations, and emerging technologies to maintain competitive advantages in your financial journey.

Banks For example, the State Bank of India provides detailed information about savings account features, interest rates, and eligibility on its official website.

Frequently Asked Questions (FAQs)

What factors should I consider when choosing bank accounts in India?

Consider interest rates, minimum balance requirements, digital banking features, customer service quality, branch networks, and additional benefits like insurance coverage and loan pre-approvals.

Which types of bank accounts in India offer the highest interest rates?

Small finance banks typically offer the highest savings account interest rates, often ranging from 6% to 7%, compared to 2.5% to 4% offered by traditional commercial banks.

Can I maintain multiple bank accounts in India?

Yes, you can maintain multiple bank accounts across different banks. This strategy helps diversify risks, optimize interest earnings, and access specialized banking services.

What is the minimum balance requirement for major banks in India?

Minimum balance requirements vary significantly: SBI requires ₹3,000 in urban areas, while HDFC Bank and ICICI Bank typically require ₹10,000. Many banks offer zero-balance accounts under specific schemes.

How do fixed deposits compare to savings accounts in India?

Fixed deposits generally offer higher interest rates (6-8%) compared to savings accounts (2.5-7%) but require money to be locked for specific periods. Savings accounts provide better liquidity but lower returns.

Are digital banking services safe in India?

Yes, digital banking services in India employ robust security measures including encryption, two-factor authentication, and fraud monitoring systems. However, customers should follow security best practices for optimal protection.

Written by Vijay Sinha

(Personal Finance Enthusiast | Helping Indians make smarter money decisions)

6 thoughts on “Complete Guide to Bank Accounts in India: Savings, FD, Minimum Balance & Interest Rates (2026)”