Understanding Credit Card Minimum Due and Its Hidden Dangers

Many credit cardholders view the SBI Credit Card Minimum Due as a convenient solution to manage their monthly payments. This option appears attractive at first—pay a small amount and avoid penalties. However, this seemingly helpful feature can create a significant financial burden if you don’t understand its implications properly.

Countless users unknowingly enter this cycle and watch their debt spiral out of control rapidly. This comprehensive guide will help you understand everything about Credit Card Minimum Due and how to use it wisely.

If you’re new to credit cards, you should also read our Complete Guide to Bank Accounts in India to understand how banking products work together.

If you’re planning your finances in 2026, you should also check the latest FD interest rates in India to understand safe investment options.

What is SBI Credit Card Minimum Due?

The SBI Credit Card Minimum Due represents the smallest amount you must pay before your due date to maintain your credit card account in good standing. When you pay this minimum amount, you achieve several immediate benefits:

Benefits of Paying Minimum Due

- Avoid late payment penalties – Your account stays current

- Keep your card active – Maintain access to credit facilities

- Preserve basic repayment history – Avoid immediate credit score damage

👉 Paying only the minimum due does not clear your total outstanding balance

👉 The remaining amount continues as debt

According to RBI guidelines on credit card billing, users must clearly understand repayment terms and interest charges.

Critical Points to Remember

The Credit Card Minimum Due payment does NOT eliminate your total outstanding balance. The remaining debt carries forward to the next billing cycle and continues accumulating interest charges.

According to Reserve Bank of India guidelines on credit card operations, financial institutions must provide clear information about repayment terms and associated interest costs.

How SBI Calculates Credit Card Minimum Due

SBI uses a comprehensive formula to determine your SBI Credit Card Minimum Due. The calculation includes multiple components beyond a simple percentage:

Components of Minimum Due Calculation

100% of the following charges:

- Goods and Services Tax (GST)

- EMI installments (when applicable)

- Various fees and penalty charges

- Applied finance charges (accrued interest)

- Over-limit amounts (if you exceed credit limit)

Plus: Approximately 2% to 5% of your remaining outstanding balance

This multi-component calculation explains why your Credit Card Minimum Due amount varies each month.

👉 This is why Minimum Due may vary every month.

You can also check the official details on the SBI Card website for accurate minimum due calculation and charges.

Real-World Example: Understanding the Impact

Let’s examine a practical scenario to illustrate how SBI Credit Card Minimum Due works:

Sample Calculation

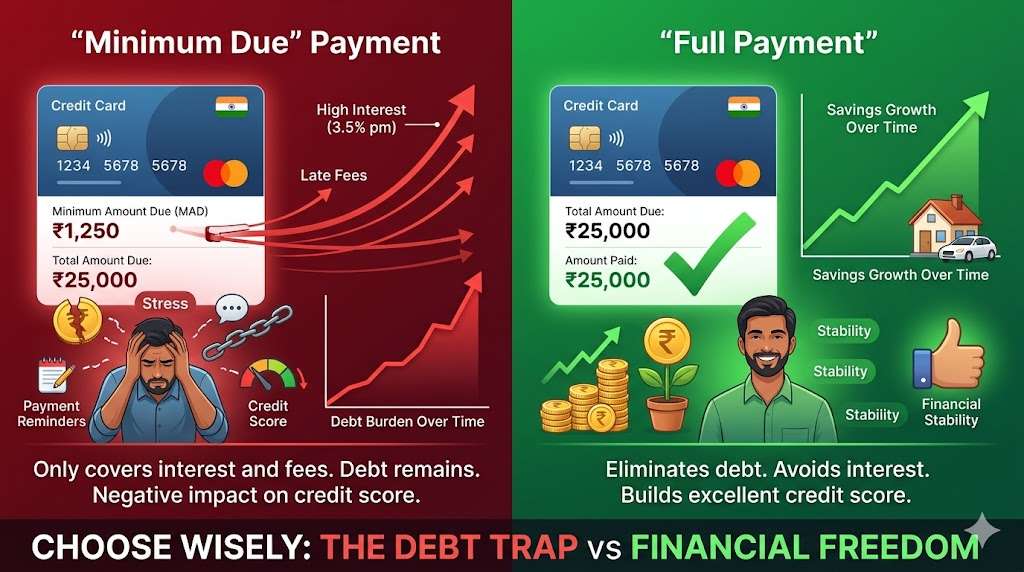

- Total Outstanding Bill: ₹50,000

- Minimum Due Amount: ₹2,000

If you pay only the minimum amount:

- Remaining balance: ₹48,000 carries forward

- Interest charges apply to the unpaid amount

- Next month’s bill increases significantly

This pattern creates substantial financial burden over time, making debt management increasingly difficult.

Hidden Dangers of Relying on Credit Card Minimum Due

1. Excessive Interest Charges

SBI credit cards typically impose approximately 3.5% monthly interest (reaching up to 42% annually) on unpaid balances. This rate ranks among the highest in personal finance products.

2. Loss of Interest-Free Benefits

When you don’t pay your full outstanding amount:

- You forfeit the grace period for new purchases

- All transactions immediately start accumulating interest

- Your financial costs increase dramatically

3. Dangerous Debt Accumulation Cycle

Regular Credit Card Minimum Due payments create a problematic pattern:

- Unpaid balances continuously carry forward

- Interest compounds monthly

- Total debt grows exponentially

- Financial recovery becomes increasingly challenging

4. Dramatic Total Repayment Increases

Small unpaid amounts can multiply quickly due to compound interest effects.

Example scenario:

Initial debt of ₹50,000 can grow to ₹70,000-₹80,000 over time when paying only minimum amounts.

5. Psychological and Financial Stress

Persistent debt creates multiple problems:

- Increased mental pressure and anxiety

- Impaired long-term financial planning

- Reduced ability to build savings

- Compromised financial security

Also read:

Credit Card Full Payment vs Minimum Due: The ₹50,000 Difference Explained

Strategic Payment Approaches for Credit Cards

Best Practices for Credit Card Management

1. Always Prioritize Full Payment

Paying your complete outstanding balance remains the optimal strategy. This approach eliminates all interest charges and maintains your financial health.

2. Reserve Minimum Due for Genuine Emergencies

Use SBI Credit Card Minimum Due only during unexpected financial difficulties—never as a regular payment strategy.

3. Convert Large Purchases to EMI

For substantial bills, consider converting them into Equated Monthly Installments at potentially lower interest rates.

4. Set Up Automatic Payments

Enable auto-pay features to:

- Prevent missed due dates

- Maintain consistent payment history

- Avoid late fees and penalties

5. Monitor Spending Patterns

Regularly track your expenses to prevent overspending and maintain control over your credit utilization.

If you’re managing multiple debts, check out our Personal Loan Guide: Interest Rates & Eligibility for better financial planning.

Comparison: Minimum Due vs. Total Due Payment

| Payment Aspect | Minimum Due | Total Due |

|---|---|---|

| Monthly Payment Amount | Low | Complete Bill |

| Interest Charges | Applied | Zero |

| Grace Period Status | Forfeited | Maintained |

| Financial Risk Level | High | Minimal |

| Long-term Cost | Expensive | Economical |

Why Credit Card Companies Promote Minimum Payments

Financial institutions actively encourage Credit Card Minimum Due payments because:

- They generate substantial interest income from unpaid balances

- Extended repayment periods increase their profitability

- Customer debt dependency creates recurring revenue streams

Understanding these incentives helps you make more informed financial decisions.

Frequently Asked Questions About SBI Credit Card Minimum Due

Can I pay minimum due every month safely?

While paying minimum due prevents immediate penalties, it results in continuous interest charges that significantly increase your total debt burden.

How does minimum due payment affect my credit score?

Short-term credit score impact may be minimal, but persistent high balances and extended repayment periods can negatively affect your creditworthiness over time.

What percentage of my bill is the minimum due?

Typically 2% to 5% of your outstanding balance, plus 100% of fees, taxes, and other charges.

Is paying minimum due a good financial strategy?

No, except during genuine financial emergencies. Regular minimum payments create expensive debt cycles.

What’s the recommended payment approach?

Always pay your complete outstanding amount to avoid interest charges and maintain optimal financial health.

For long-term financial growth, you can also explore our Mutual Funds Guide for Beginners.

Conclusion: Smart Credit Card Management

SBI Credit Card Minimum Due may appear convenient, but regular reliance on this option creates significant financial risks. Understanding the true cost of minimum payments helps you make better decisions about credit card management.

Key takeaways for financial success:

- Always aim to pay your full outstanding amount

- Use minimum due only during genuine emergencies

- Monitor your spending to prevent excessive debt accumulation

- Consider EMI options for large purchases when necessary

By following these principles, you can enjoy the benefits of credit cards while avoiding the expensive trap of persistent debt accumulation.

Thanks a lot for your comment. I’m glad the article helped you understand the topic better. Stay connected for more updates.