EPFO plans to roll out EPF withdrawals via UPI by April 2026. Discover how this amazing move will make PF withdrawals faster, easier, and paperless, along with eligibility rules, benefits, timelines, and what EPF members need to know.

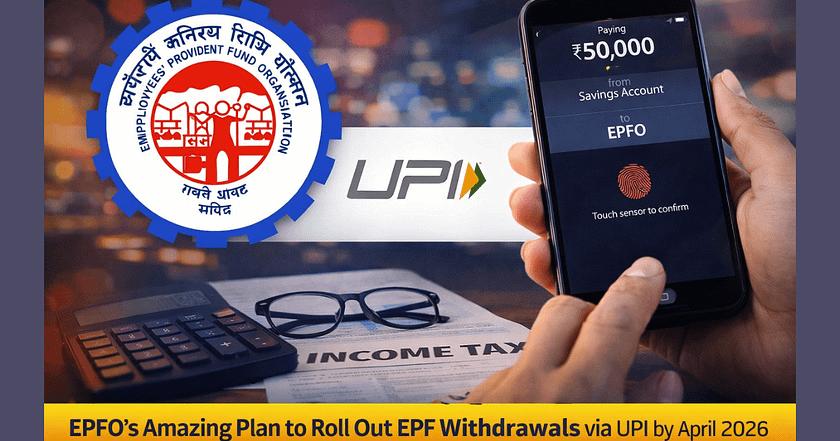

You might soon be able to receive your Employees’ Provident Fund money as easily as you pay for coffee. The Employees’ Provident Fund Organisation (EPFO) has announced that **EPF withdrawals via UPI** should become a reality by April. For finance enthusiasts who track every new personal-finance perk, this is big news. In this guide, we’ll explore what the change means, how it will work, and what you should watch out for once the option goes live.

“From a seven-day wait to a few screen taps—UPI could become the shortest distance between your EPF account and your bank balance.”

Why the EPFO Is Betting on UPI: EPF Withdrawals via UPI by April 2026

Unified Payments Interface (UPI) has become India’s favourite way to send and receive money. So why did it take this long for EPFO to join the party? Let’s break it down.

The growth story of UPI

* Over 11 billion transactions were logged in January 2024 alone.

* UPI handles more value each month than credit cards and debit cards combined.

* The system is available 24/7, costs almost nothing per transaction, and plugs into every major bank.

EPFO’s current payout pain points

1). Time lag:

Even with online claims, it can take three to seven working days for funds to reach members.

2).Bank validation:

EPFO has to verify bank IFSC codes and account numbers—a process prone to delays.

3).Failed credits:

Inaccurate account details routinely bounce back PF payouts, triggering manual rework.

By linking EPF withdrawals to UPI IDs, EPFO hopes to compress settlement time to a matter of minutes, lower failure rates, and trim operational effort.

How EPF Withdrawals via UPI Will Work: EPF Withdrawals via UPI by April 2026

The core change is simple: instead of entering a bulky bank account number and IFSC, you will enter your UPI ID (for example, `name@bank`). The rest of the steps remain almost identical, but the back-end rails differ. Here’s a step-by-step walk-through for the curious.

Filing the claim

1. Log into the EPFO Member e-Seva portal.

2. Pick “Claim” under the “Online Services” menu.

3. Select the type of withdrawal—full, partial, advance, or pension withdrawal.

4. When prompted for payout details, choose “UPI” and type your UPI ID.

What happens behind the scenes

* EPFO’s system pings the National Payments Corporation of India (NPCI) to validate the UPI handle.

* Once validated, an immediate payment request is created.

* Your bank or payment app sends you a message—“₹X has been credited from EPFO.”

* Because UPI is real-time, the funds reflect in your linked account instantly.

Safety checks in place

* Only verified UPI handles approved by NPCI will be accepted.

* EPFO will continue Aadhaar-based e-KYC to confirm member identity.

* A dual-factor check—Aadhaar + UPI validation—should reduce fraud risk.

Potential Benefits for Members: EPF Withdrawals via UPI by April 2026

Faster access to money

The biggest win is speed. Think about scenarios like medical emergencies or home loan repayments where every day counts. Instead of waiting for end-of-day NEFT or next-day RTGS, **EPF withdrawals via UPI** could land within minutes after approval.

Lower rejections

UPI IDs rarely change and are easier to type than a 15-digit bank account plus IFSC. Fewer typos mean fewer rejected claims.

Convenience for job hoppers

People who change jobs often forget to update bank details in their PF records. A single UPI handle stays valid even if you switch banks, making life simpler.

Possible Snags to Watch Out For

Nothing in finance is flawless. Before you rely fully on the new route, keep these caveats in mind:

1). UPI limits:

Most apps cap daily incoming transfers at ₹2 lakh. Higher EPF withdrawals may still route through the old bank-transfer method.

2). Multi-factor approvals:

Your company’s digital signature on Form-19 or Form-31 remains mandatory. UPI doesn’t bypass that requirement.

3). Linking issues:

If your UPI ID is tied to a non-bank wallet, EPFO may reject it in the first phase; banks might be whitelisted first.

What Employers Need to Do: EPF Withdrawals via UPI by April 2026

Update internal HR processes

* Ensure that your HR portal collects employees’ UPI IDs securely.

* When verifying exit documentation, cross-check that the UPI ID matches the Aadhaar name spelling to avoid validation failure.

Communicate changes to staff

HR teams should send clear instructions:

* A checklist on how to find one’s UPI ID in common apps (PhonePe, Google Pay, Paytm, etc.).

* A FAQ on limits, privacy, and fallback options.

* Timelines: EPFO targets April, but ERP systems may need their own testing.

Frequently Asked Questions

Q. Will UPI work for international bank accounts?

A. No. UPI is an India-only rail. NRIs will still need to use NEFT/RTGS to an NRO or NRE account.

Q. Can I use multiple UPI IDs?

A. EPFO will allow only one validated UPI ID at a time. You can update it later if needed.

Q. Does this affect my regular PF contributions?

A. No. Contributions remain untouched. The change is only for outward payments (withdrawals, pension, insurance).

How to Prepare Before April

1). Verify KYC on the Member e-Seva portal.

Incomplete KYC is still the top reason for claim rejections.

2). Create a UPI ID linked to your salary account.**

This keeps things tidy when reconciling credits.

3). Check daily UPI limits with your bank.**

Request a higher inward limit if you foresee a large withdrawal.

4). Follow EPFO’s official social channels.**

That’s where pilot launch dates, downtime notices, and step-by-step videos will appear first.

The Larger Impact on India’s Fintech Landscape

EPFO manages over ₹20 lakh crore in retirement funds. Even if only a small slice of monthly payouts shifts to UPI, it will:

* Test UPI’s capability for high-value, high-volume government transactions.

* Encourage other social-security bodies (ESIC, PFRDA) to consider similar moves.

* Strengthen the case for widening UPI limits beyond ₹2 lakh.

Industry insiders predict the feature will push UPI deeper into “financial-services rails” rather than just retail payments.

Parting Thoughts: EPF Withdrawals via UPI by April 2026

EPF withdrawals have always been notorious for paperwork and waiting periods. By offering **EPF withdrawals via UPI**, EPFO could change that reputation in one stroke. The initiative combines real-time settlement with the widest payment network in the country. As finance enthusiasts, we should keep a close eye on the April rollout, test the waters with a small advance claim if possible, and share feedback to iron out the kinks.

“If this succeeds, your retirement money will be just a few taps away—no forms, no queues, no missed deadlines.”

Are you ready to add your UPI ID to your EPF profile? The countdown to April has begun.

Also Read-

https://topupdates.in/8-percent-fd-rates-for-seniors/

https://topupdates.in/zomato-online-food-delivery-coupon-hacks/

https://topupdates.in/7-key-changes-in-epf-rules-old-vs-new-rules/